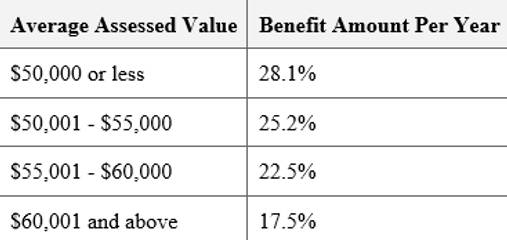

Owners of cooperative units and condominiums who meet the requirements for the Cooperative and Condominium Property Tax Abatement can have their property taxes reduced. The amount of the abatement is based on the average assessed value of the residential units in the development. Abatement percentages are as follows:

Requirements

- Co-op and condo boards and managing agents must notify the Department of Finance of changes in ownership or eligibility for the Cooperative and Condominium Property Tax Abatement by February 15, or the following business day if February 15 falls on a weekend or holiday.

- New condominium owners must have filed a real property transfer tax (RPTT) form or deed with the Division of Land Records at www.nyc.gov/acris. For more information, visit the Real Property Transfer Tax page.

- The co-op or condo unit must be the owner's primary residence. Co-op shareholders and condo unit owners: Please tell your board or managing agent if the unit is your primary residence so that you can receive the abatement.

- You must have purchased the unit on or before January 5 to qualify for the abatement for the upcoming tax year. If the unit was purchased after January 5, you can apply for the next tax year.

- Co-op or condo owners cannot own more than three residential units in any one development and one of the units must be the owner’s primary residence.

- Property must be classified as a tax class 2 property.

- Properties that are part of the Urban Development Action Area Program (UDAAP) cannot receive the abatement.

-

J-51 exemption

-

420c, 421a, 421b, or 421g

-

The clergy property tax exemption

The co-op or condo property cannot be:

-

a Housing Development Fund Corporation (HDFC);

-

a Limited Divided Housing Companies, Redevelopment Company;

-

a Mitchell-Lama Building or

-

in the Division of Alternative Management Programs (DAMP) Program.

-

Units owned by a business (LLC) are not eligible.

-

Units held by sponsors or their successors in interest are not eligible.

-

Units owned by a trust are eligible only if the unit is the primary residence of the beneficiary of the trust, trustee, or life estate holder. All beneficiaries must have the unit as their primary residence in order to be eligible for the abatement.